Looking at taking a position in a new company, CPT Global, CGO.

CPT Global Limited is a specialist IT consulting services firm. They claim to operate in 3 divisions,

transformation - leveraging technology for business success.

assurance - assured, reliable delivery & operations

optimisation - faster, more efficient technology

From their website,

"CPT Global Limited is a highly regarded, specialist IT consulting services firm with a reputation built over successful engagements across the globe. CPT has been engaged by 80% of the world�s largest banks. We have delivered outcomes and engagements for clients across 35 countries.

CPT is an established business with a high-profile customer base, including a number of Fortune 500 companies. In our home market of Australia, CPT has a strong and stable position in the professional services segment of the Australian information technology market. CPT has experience working for federal and state government in Australia as well as banking, finance, insurance, telecommunications, retail and manufacturing sectors both in Australia, as well as globally. We partner with world leading technology organisations to bring unique value to our clients."Its tightly held with just under 70% held by the top 20 and the founder & family holding about 30%.

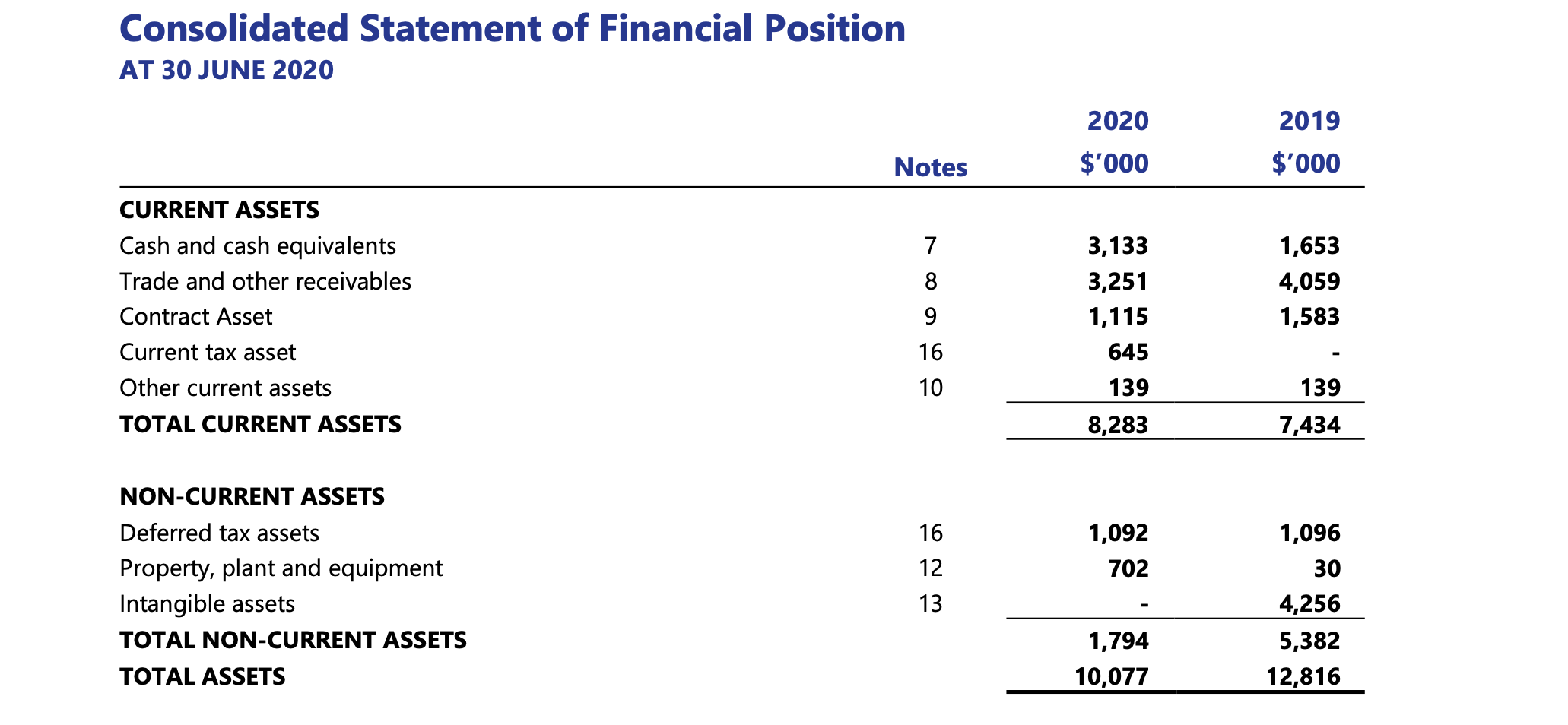

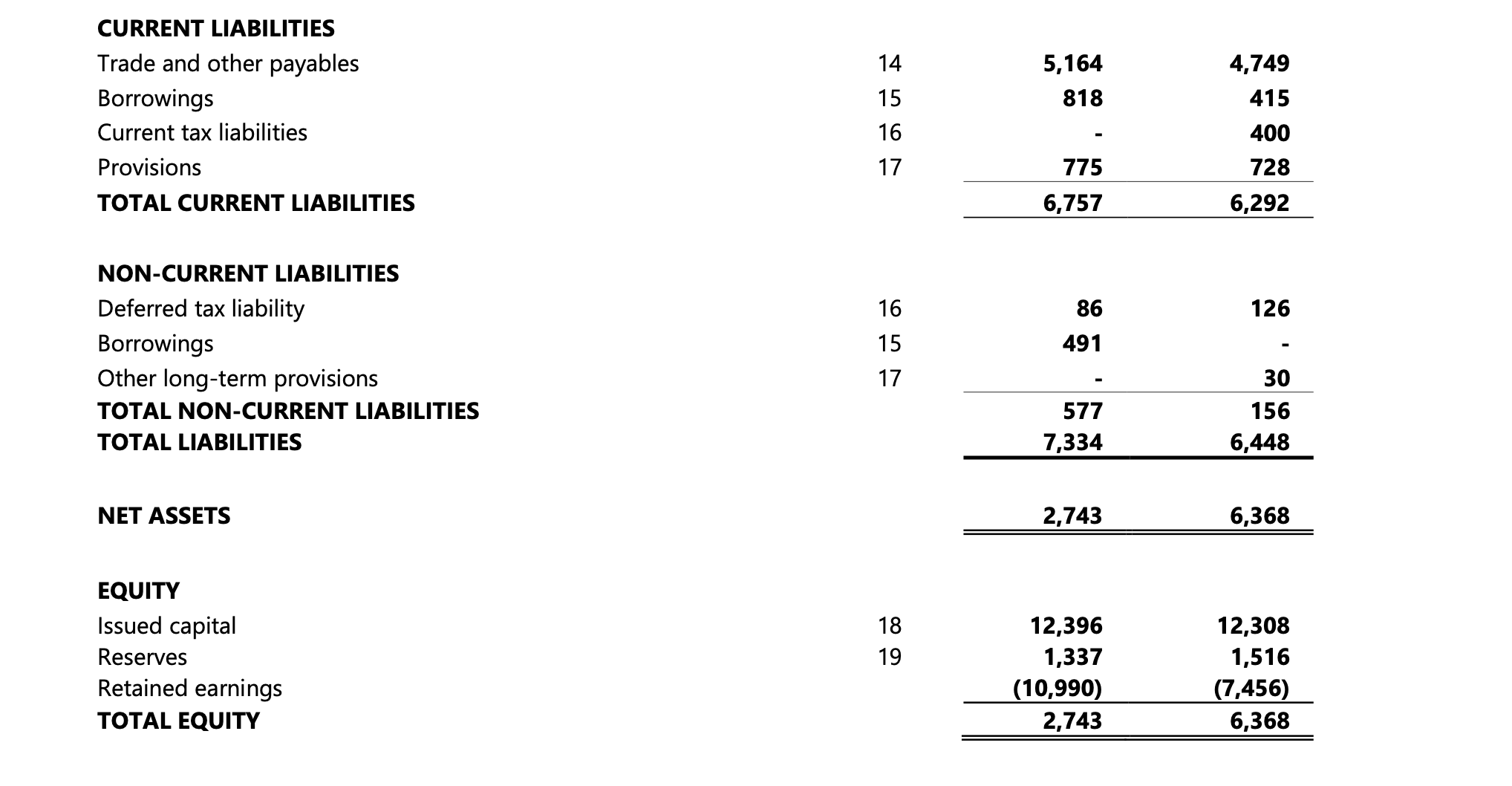

Basically its an incredibly capital light business, they chose to impair all their existing goodwill last finanacial year which further simplified the balance sheet,

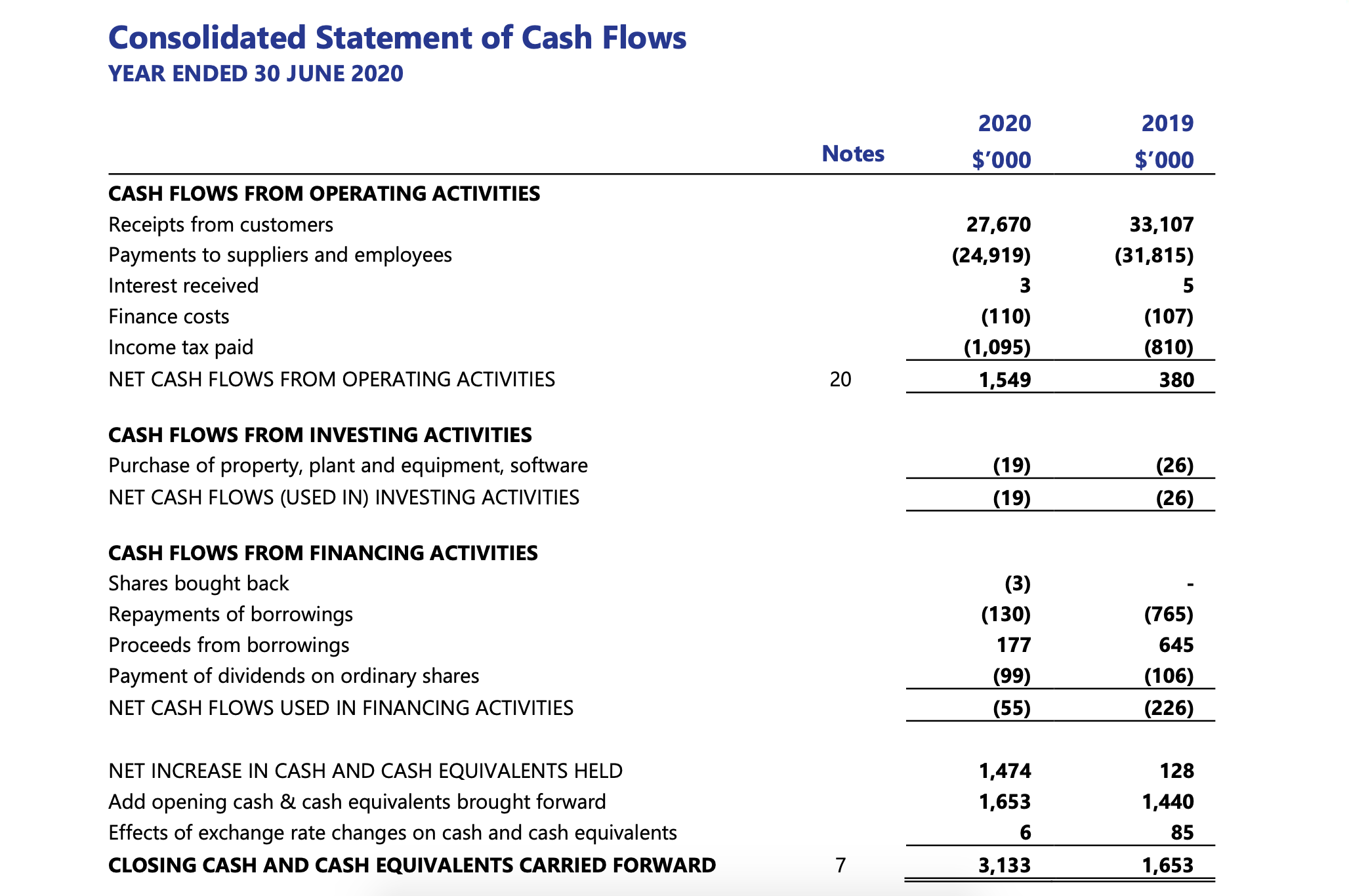

Cash flow is also very clean, pretty obvious that any incremental growth will drop to the bottom line.

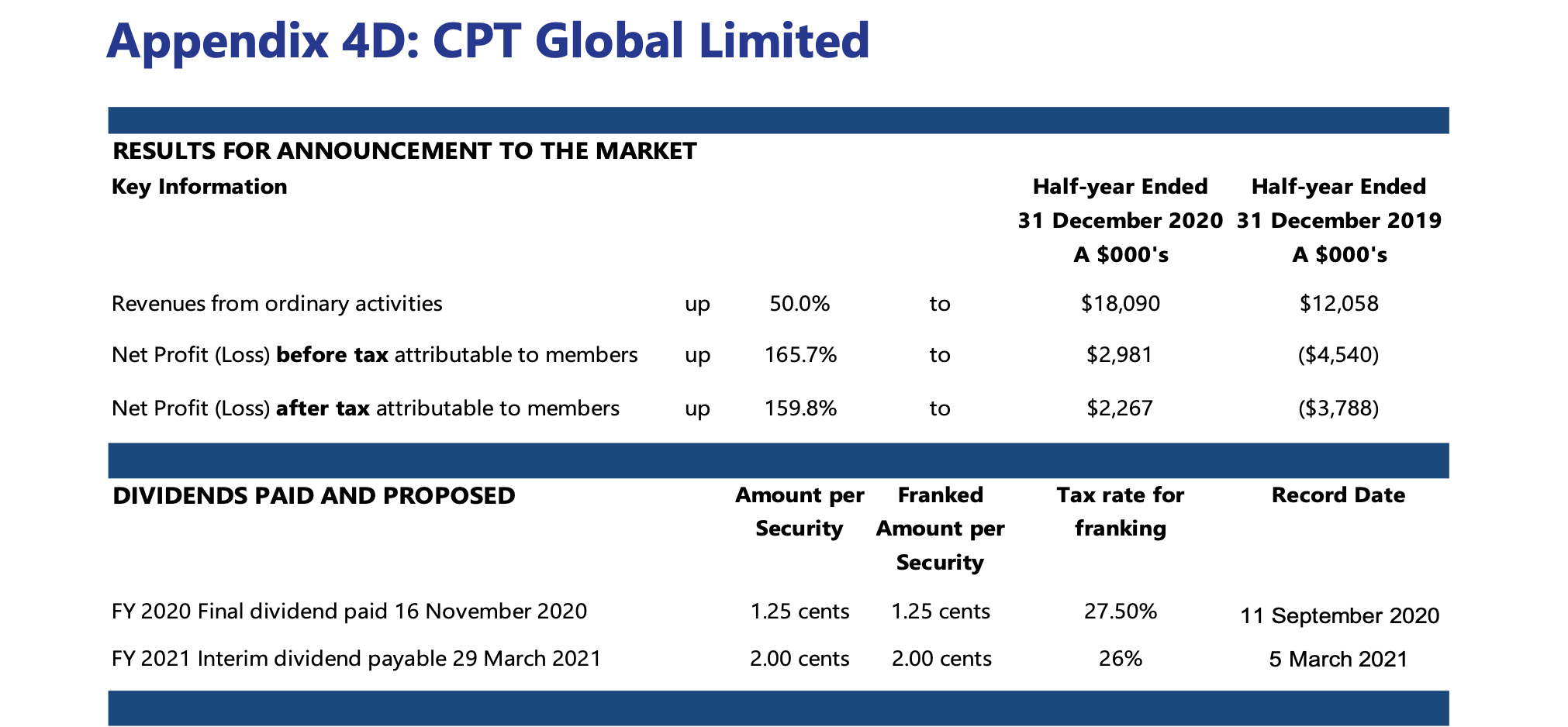

Moving onto the H1 2021 and results have really taken off, largely driven by covid & the impact on businesses with WFH and extra IT capability, so probably a high point at current trajectory and I would expect some slowing of growth for the 2nd half and 2022. Regardless the numbers are extremely good and make the business look extremely cheap.

My back of the envelope numbers are the business should be able to make around $4m NPAT $2.8m FCF for the full year. Market cap at 50c is around $20m, and EV about $17m. So on that basis its trading at around 5x earnings and 7x FCF which looks remarkably cheap. EV/EDITDA is around 3 based on annualised EBITDA from H1.

FCF is about 4.3c for the half so if we assume 8c for the full year then my quick and dirty range of valuation is over $1

Inversely, for a price of 50c to be fair value by my calculation FCF would have to drop to 3c for the full year. Fairly unlikely given its already made over 4c for the half!

My discussion with Luke about it,

Hi Luke, just wondering if I could pick your brains on $CGO. Not sure how I havent picked this one up in one of my screens given its metrics, but somehow I had not heard of it until you mentioning it this week. I have had a look back thru its reports and even after yesterday's price pop it looks extraordinarily cheap. Which makes me think, what am I missing?! I think the impairment last year was very impressive, a lot of management would have avoided or half done the job, to get all the goodwill off the balance sheet has really impro ved the financials looking thru the results going forward. Any way I look at it, the business looks robust, basically no debt, strong FCF, clean earnings, good yield, clients worldwide, even with very modest growth its looks like a company I would love to own! Strong founder ownership too with founding family and directors holding about 30% which I always like to see. Back of the envelope I can buy the whole business for $20m on probably $4m NPAT for the full year. That seems pretty compelling to me!!

So whats the bear case? Why is anyone selling shares if its so good? So far I havent thought of any obvious catastrophic risk. Other than market risk I cant really think of anything as a negative - which is unusual for me. Cheers, RIck

...one thing that is a bit jarring is the claims of "engaged by 80% of the world�s largest banks." - that seems a big claim for a tiny company! Makes me wonder what the engagement actually is, hard to see it generates much revenue! Thats the only thing thats twitched my radar so far.

Hey mate, you've done a pretty good job of hitting all of the positives. Agree with all that. The two criticisms I see is whether it crosses the line from strong founder ownership into lifestyle company. I've been told that many years ago it was a much more popular stock than it is today with a few small funds in it and they were excited by a new CEO who was brought in with big tech experience from the US, only for a year or two later to resign and the Exec Chairman to appoint his son as US General Manager. In a nutshell, question over whether they act in minority shareholders interests. Some scuttlebutt, but when I spoke with them it was shortly after RXP got acquired for 7x EBITDA and the Chairman was very annoyed at their multiple in comparison. Maybe that will give him the kick up the bum to focus harder on earning and possible engage with the market again. Either way, my response to that criticism is whatever happens you will get your share of the divi, which is a bloody solid return on its own.

Second negative is they are in a lumpy industry. IT services at the mercy of short term contracts. Mitigated somewhat by large customers, but nonetheless genuine. The growth in this result isn't sustainable, they are coming off a low base and their core competency of database efficiency was in vogue with work from home due to Covid. Still, I feel like $4-5m is sustainable earnings with the current business and even single digit revenue growth should do well because it's a scalable business through to profits. Clean accounting, great cash conversion supports high dividends, I really like it

Also they were smart enough to pullback, but expansion into UK/EU didn't go well. All of their operating tax losses are in the UK